The core activity of manufacturing companies is to produce. The sound management of the production cost should thus be at the very center of their financial operations. Similarly, service organizations implement efficient methods to better understand the cost of the services they offer.

_edited.jpg?width=600&name=DAMASIX%20DMS%20Daily%20management%20gestion%20quotidienne%20(1)_edited.jpg)

A Glance at Createch’s Performance Initiatives

For 25 years, Createch’s mission has been to significantly improve its clients’ profitability through highly collaborative consulting procedures aiming to optimize business processes, based on Lean management principles. Our approach involves developing practices best suited to your situation, in compliance with a proven methodology, including:

- Diagnosing the current end-to-end performance of processes;

- Identifying performance variations and waste sources;

- Defining a future strategy, and projects that will help to reach said strategy’s targets.

A classic accounting structure brings about very little support to Performance initiatives.

Our service offer in financial performance improvement (Lean accounting or Lean finance) is based on your value creation vectors. Beyond optimizing your finance processes and maximizing the efficiency of your production cost system, this approach is designed to provide relevant information to identify and keep a record of waste sources. Your finance department will play a proactive role as your business partner!

Alarming Symptoms of a Failing Production Cost System

Many symptoms indicate a failing production cost system:

- Opaque profit margins;

- Fragmentary information to promote or remove certain products;

- Difficulty in identifying poorly performing activities;

- Lengthy analyses and uncertain results;

- Poorly integrated technology tools.

Defining Production Costs

Many confuse production cost with total cost. Total cost is the overall costs to sell and distribute a product or service to a customer. It includes procurement costs, production costs as well as marketing and distribution expenses.

The production cost, on the other hand, is used to provide a detailed assessment of the costs expected or incurred to produce a material (product) or offer a service. Good knowledge of these costs’ behaviour allows for better control of the profit margin and identification of waste. Beyond generating reports and assessing inventory, the production cost ultimately aims at providing accurate information to improve manufacturing performance, raise productivity issues, and identify waste sources and non-productive times.

People often mistakenly consider that improving only the parameters used to calculate the production cost is enough to get reliable analyses. It is best—even so imperative—to optimize the plant’s operations and to adjust the parameters that feed the production cost system.

The production cost is the finance layer supporting manufacturing operations. The optimization of work floor operations and that of production cost system parameters go hand in hand in the pursuit of continuous and efficient improvement. Experienced businesspeople leverage this for better decision-making.

Calculating the Production Cost

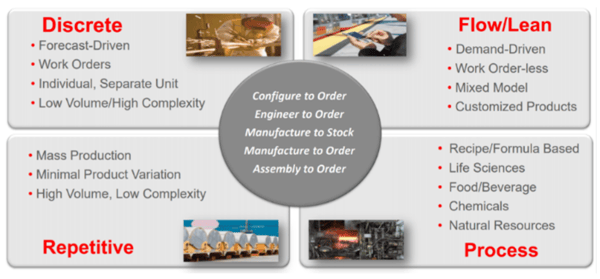

Each organization has its own distinctive characteristics. Different manufacturing processes respond to different needs. It is important to be aware of the differences between these processes, especially since the production cost should reflect the behaviour of process-specific costs.

The most common manufacturing processes are:

- Mass production

- Process mode

- Discrete or workflow mode

- Line production (repetitive mode)

- Intermittent production (flow or Lean mode)

- Custom production

In process or discrete mode, a chain of successive work cells constitutes a production line. For the same material to be produced, production orders are distributed among the various production steps. Each work cell conducts specific activities determined in accordance with the work instructions, and the recipe for the production order. The production cost system should make sense of the specifics of each manufacturing process, and of the performance characteristics of each production line.

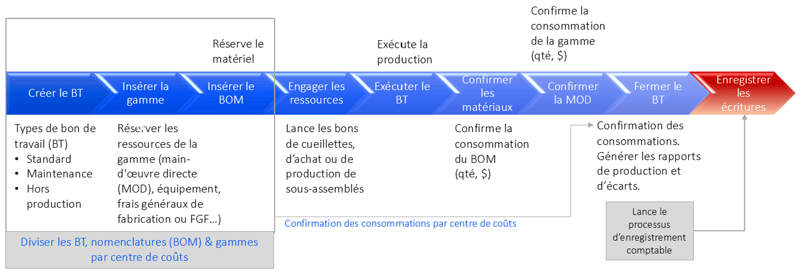

A production order usually includes the following basic steps:

Each production order is linked to a routing and to a bill of materials (BOM). The generic routing, which comprises work instructions, labour time and machine time, is divided between each work cell. The BOM, which lists all materials and components required, is also distributed among the work cells. The production order, routing and BOM together constitute the data sheet of a given material to be produced.

The production cost should take into account the behaviour of the cost consumed at each step of the production order, identify the variations between projected cost and actual cost, valuate manufactured goods, and report on waste sources.

Createch offers a range of services for the improvement of your operational and financial performance, with an expertise relying on advanced technology solutions such as SAP ERP, SAP WMS, SAP EPM, DELMIA Ortems (APS), and Damasix (DMS). Contact one of our experts for more information!